FORM 1 – INDIVIDUAL SUBSTANTIAL SHAREHOLDER

NOTICE

General Notes

1.

This

Form 1 is for use by an individual disclosing a notifiable interest in a Hong Kong listed

corporation under Part XV of the Securities and Futures

Ordinance (Cap. 571) (“SFO”)

who is not a director or chief

executive of the listed

corporation. Form 3A should

be used by a person who is a substantial

shareholder and also a director or chief executive of the listed corporation concerned (see the Special Notes on page 11). You

must complete the notice in accordance with the directions and instructions in these Notes

and then file the notice with The Stock

Exchange of Hong Kong Limited (“SEHK”).

2.

Use :

Form 2 if you are a corporation with an interest of 5% or more of the voting shares of a listed corporation making a disclosure.

Form 3A if you are notifying interests in shares of the listed corporation of which you are a director or chief executive.

Form 3B if you are notifying interests

in shares of any associated

corporation of the listed corporation of which you are a director or chief executive.

Form 3C if you are notifying interests in debentures of the listed

corporation of which you are a director or chief executive.

Form 3D if you are notifying interests in debentures of any associated corporation of the listed corporation of which you are a director or chief executive.

Form 4 if you

are a listed corporation that is required by section 330(1) or 333(1) of the SFO

to notify the SEHK of information received in pursuance of a requirement

imposed by the listed corporation under section 329 of the SFO, or to deliver a

report prepared under section 332 of the SFO to the SEHK.

3.

Please use separate forms to disclose your interest if you are interested in

(i) more than one class of

voting shares of the listed corporation, or shares or debentures of a listed corporation of which you are a director or chief executive,

and shares or debentures of an associated corporation of such listed

corporation; or (ii) shares or debentures of more than one associated

corporation of a listed corporation of which you are a director or chief

executive. Chinese versions of these forms are also available.

Meaning of “notifiable interest”, “shares”, “substantial shareholder” and “you” in these Notes

4.

A “notifiable interest” is an interest

of 5% or more of the voting shares of a Hong Kong listed

corporation (in Form 1 and these Notes shortened to “shares”).

Form 1 and these Notes use the term “substantial shareholder” to describe a person

with a notifiable interest. In these Notes the word

“you” refers to the substantial

shareholder.

“Relevant event” and “Initial Notification”

5.

You must give notification of interests in shares of a listed

corporation, and any “short position” (explained in General Note 12 below) on the occurrence of certain events - called “relevant events”

(see section 308 of the SFO). Relevant events include :

(i)

When you first become interested in 5% or more of the shares of a listed corporation (i.e. when you first acquire a notifiable interest).

(ii)

When your interest

drops below 5% (i.e. you cease to have a notifiable interest).

(iii)

When there is an increase or decrease in the percentage figure of your holding

that results in your interest crossing over a whole percentage number which is above 5% (e.g. your interest increases from 6.8% to 7.1% - crossing over 7% or it decreases from 8.1% to 7.8% crossing over 8%).

(iv)

When you have a

notifiable interest and the nature of your

interest in the shares

changes (e.g. on exercise of an option) (see further below).

(v)

When you have a notifiable interest and you come to have, or cease

to have, a short position of more than 1% (e.g. you are already

interested in 6.8% of the shares of a listed corporation and write, issue or

become the holder of an equity derivative under which you have a short position of 1.9%).

(vi)

When you have a notifiable interest and there is an

increase or decrease in the percentage figure of your short position that results

in your short position crossing over a whole percentage

number

which is above 1% (e.g. you are already interested in 6.8% of the shares of a listed corporation and increase your short position from 1.9% to 2.1%).

(vii)

If you have an interest in 5% or more of the shares of a corporation that is being listed, shares of a class that is being listed,

or shares of a class which are being given full voting rights.

(viii)

If the 5% threshold is reduced (and

you have a notifiable interest immediately after the reduction) or the 1 %

threshold for short positions is reduced (and you have a notifiable interest

and a short position that is notifiable immediately after the reduction).

A notification of relevant events (vii) and (viii) is described in Form 1 and these Notes as an “Initial

Notification”.

Relevant event (iv) may

not always give rise to a duty to give a notification. The change in the nature of your interest is not

required to be reported if the percentage level (see General Note 7) of your

interest that has not changed, and the percentage level of your interest

at the last notification given by you are both the same. For example, if you

have an interest in 5.6% of the shares of a listed corporation and lend 0.5%

the percentage level of your interest that has not changed is 5.0% (i.e.

5.6% less 0.5% equals a percentage figure of 5.1% which is then rounded down to

a percentage level of 5.0%) and no notification need be made. However, if you have an interest in 5.6% of

the shares of a listed corporation and lend 1.0% the percentage level of your

interest that has not changed is 4.0% (i.e. a percentage figure of 4.6% rounded down to a percentage level of 4.0%)

and a notification must be made.

Timing of notification

6.

In

the case of events (i) to (vi) in General Note 5, you must give the notification

within 3 business days of the day you became aware of the relevant event. The term “business day” means a day other than a

Saturday, a public holiday and a day on which a black rainstorm warning,

or a gale warning, is in force. The period is calculated excluding the day that the relevant

event occurred.

For

an Initial Notification, you must normally

give the notification on this Form 1 within 10 business days after the relevant event. However, if at that date you were not aware that you had a notifiable

interest, or a short position, then you must give the notification within 10 business days of the day you became aware that you had such an interest or short position.

The period allowed for filing a notice runs from the time you know of the facts that constitute the event (e.g. the purchase of the shares, the delivery of the shares, the buy back of shares by the listed corporation), not the day that you realize that the event gave rise to a duty of disclosure under Part XV of the SFO.

Working out the percentage figure of your interest

7.

In

Boxes 15 and 16 of Form 1 you are asked to state the percentage

figure of your interest

in shares of the listed corporation. To work this out you express the total number of shares in which you are interested as a percentage of the number of shares of the listed

corporation, of the same class, in issue (i.e. the number in Box 6). Round this figure to two decimal places. To work out the percentage level of your interest you simply round down the percentage

figure of your interest

to the next whole number.

8.

In

calculating the total number of shares

in which you are interested

you must include all joint interests (see Specific Note to Box 21 below), interests through equity derivatives

(see General Note 10 below) and any such interests

in shares of the same listed corporation that any of the following persons and trusts have :

(i)

Your spouse and any child of yours under the age of 18 (see

Specific Notes to Box 19);

(ii)

A corporation which you control (a corporation is a “controlled

corporation” if you control, directly or

indirectly, one-third or more of the voting power at general meetings of the

corporation, or if the corporation or its directors are accustomed to act in

accordance with your directions) (see

Specific Notes to Box 20);

(iii)

A trust, if you are a trustee of the trust (other

than a trust where you are a bare trustee i.e. where you have no powers or

duties except to transfer the shares according to the directions of the

beneficial owner) (see Specific Notes to Box 22);

(iv)

A discretionary trust, if you are the “founder” of the trust (e.g.

you had the trust set up or put assets into it), and can influence how the trustee exercises his discretion (see

Specific Notes to Box 22);

(v)

A trust of which you are a beneficiary (discretionary interests may be ignored); or

(vi)

All

persons who have agreed to

act in concert to acquire

interests in shares in the listed corporation, if you are a party to the agreement (see Specific Notes to Box 23).

9.

You must also count as your short position any short positions that the persons and trusts mentioned in General Note 8 have. This may create a short position (if you do not have a short position already) or increase

the size of your short position.

10.

In

calculating the percentage figure of your interest in shares you must add together both direct and indirect

interests. You

must not net off long positions and short positions but must disclose

them separately.

Indirect interests include interests

in shares underlying “equity derivatives”.

Equity derivatives include instruments such as options, warrants,

stock futures and are referred to in these Notes as “derivatives”. “Underlying shares” are the shares

that may be required to be delivered to you, or by you, under the derivatives,

and include the shares used to determine the price or value of the derivatives (e.g. in the case of an issue of “European Style Cash Settled

Call Warrants 2001-2002 relating

to ordinary shares of HK$10.00 each in XYZ Ltd. issued by ABC Investment

Bank” the “underlying shares” are ordinary shares of HK$10.00 each in XYZ Ltd.).

“Long positions” and “short positions”

11.

You have a “long position”

if you have an interest in shares, including interests through holding, writing or issuing financial

instruments (including derivatives)

under which, for example :

(i)

you have a right to take the underlying

shares;

(ii)

you are under an obligation to take the underlying shares;

(iii)

you have a right to receive from

another person an amount if the price of the underlying shares is above a

certain level;

(iv)

you are under an obligation to pay another

person an amount if the price of the underlying shares is below a certain

level; or

(v)

you have any of the rights or obligations referred to

in (i) to (iv) above embedded in a contract or instrument.

12.

You have a “short position” if you borrow shares under a securities borrowing and lending agreement, or if you hold, write or issue financial instruments (including derivatives)

under which, for example:

(i)

you have a right to require another person to take the underlying shares;

(ii)

you are under an obligation to deliver the underlying shares;

(iii)

you have a right to receive

from another person an amount if the price of the underlying shares is below a

certain level;

(iv)

you have an obligation to pay another person an amount

if the price of the underlying shares is above a certain level; or

(v)

you have any of the rights or obligations referred to

in (i) to (iv) embedded in a contract or instrument.

13.

The

number of shares in which you are taken to be interested, or to have a short position, through derivatives is:

(i)

the number of shares that may have

to be delivered to you, or by you, on the exercise of rights under the

derivatives;

(ii)

the number of shares by reference to which the amount payable under the derivatives is derived or determined; or

(iii)

(in the case of stock futures contracts)

the contract multiplier times the number of contracts you hold.

If any party to a derivative

can choose whether

to settle in cash or by delivery then use (i) to work out the number of shares in which you are interested. If it is not possible to determine precisely the number of shares in which you are taken to be interested

(or have a short position)

at the date when you

first acquire an interest in the underlying shares

through an equity derivative then you should still file a notice

if the number of shares in which you are interested may exceed 5% or more of

the issued shares of the listed corporation concerned. For example, if the number of shares that you will

receive under an equity derivative is determined by the price of the shares on

a given date in the future (and there is a minimum number that you are bound to

get) then if that minimum number (together with any other shares in which you

are interested) exceeds 5% or more of the issued shares of the listed

corporation concerned, a duty arises on entering into the derivative. If the derivative specifies only a maximum,

then disclose the maximum figure. If the

derivative specifies both a maximum and a minimum, then disclose the figure

which is most appropriate. If the derivative does not specify any minimum

or maximum,

then no duty of disclosure arises on entering into the derivative. Once the number of shares that you will receive is known a duty of disclosure arises.

General

14.

The

“Outline of Part XV”

(“Outline”)

published by the Securities and Futures Commission (“SFC”)

gives further guidance

on the situations in which a notice will have to be filed under Part XV. A copy of the Outline can

be downloaded from the SFC’s website http://www.sfc.hk. However, when making a disclosure you must satisfy yourself of the requirements of the SFO, and if in doubt, please seek appropriate legal advice.

Electronic filing of notices

15.

Upon the commencement of Part 4 of the Securities and

Futures (Amendment) Ordinance 2014 on 3 July 2017 (“Commencement”), you should

file this Form 1 electronically with SEHK by using the Disclosure of Interests

Online System (“DION System”) from HKEX website https://sdinotice.hkex.com.hk. Upon Commencement, other than in the

circumstances set out in paragraph 19 below, filings sent by fax, by post, by

email or delivered by hand will not be accepted and will not be in compliance

with the requirements under Part XV of the SFO.

16.

Forms are available

in Adobe Portable Document format (“PDF”) or in Microsoft Excel format. If

you are a Windows user, you may download and file a notice using either

format. If you are a Mac user, you may

only download and file a notice in PDF.

You may download a soft copy of this Form 1 (and these Notes) for

completion from HKEX website at https://sdinotice.hkex.com.hk

or the SFC website http://www.sfc.hk/web/EN/rule-book/sfo-part-xv-disclosure-of-interests/di-notices.html. If you download this Form 1 from the HKEX website,

you can either download (i) a complete blank Form without logging in the DION

System; or (ii) a blank Form prefilled with certain profile information after

logging in the DION System. You can only

download a complete blank Form from the SFC website. If you are using Excel format, you must

click "Enable Content" when opening the Excel forms - otherwise the

macros will not work. If you are using

PDF, you must click “Trust this document always” and save the changes.

17.

You are also required to separately submit this Form 1

to the listed corporation concerned but SEHK will send this Form 1 to the

listed corporation on your behalf if you complete and file this Form 1

properly. The completed Form 1 that you

filed with SEHK will be sent to the listed corporation concerned based on the

stock code and the date of relevant event on the Form. Based on the stock code on the Form, the

system will fill in the name of the listed corporation. If you decide to state a corporation name

which is different from what is suggested by the system, there is a risk that

the system is not able to associate the corporation name with the relevant

stock code and thus fails to direct your Form to the relevant listed

corporation.

18.

Do not send copies

of

share purchase agreements

and other documents to SEHK when filing this Form 1 (except in

relation to copies of concert party

documents as indicated in the Specific Notes to Box 23).

Attaching a document that explains the transaction in question does not discharge the duty to complete the prescribed form. Unless

otherwise stated, copies of any documents that are sent to SEHK will be displayed together with this Form 1 on

HKEX website http://www.hkexnews.hk/di/di.htm and be

available for viewing by the public when searching the DI pages of the HKEX

website.

19.

If your duty to file a notification on Form 1 arose

before the date of Commencement, you may either (i) submit this Form 1 to SEHK by

using the DION System; or (ii) submit the prescribed Form 1 available for use

immediately before the date of Commencement to SEHK by fax, by post, by email

or by hand. All filings made after the

period of 3 months from the date of Commencement should be made by using the

DION System.

Specific Notes

A substantial shareholder

who

is also a director or chief executive of the listed corporation concerned should read the Special Notes on page 11. An approved

lending agent (“ALA”) or the holding company of an ALA should also read the

Special Notes on pages 11-12.

|

Box 1 |

State the date of the relevant event (explained in

General Note 5) which gave rise to the notice. |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Box 2 |

In the case of events (i) to (vi) in General Note 5,

if you became aware of the relevant event on a date later than the date that

it occurred, then state the date that you became aware of the event that

triggers the reporting obligation in Box 2. For an Initial Notification, if you were not aware

that you had an interest, or a short position, at the date of the relevant

event, or were not aware that you had 5% or more of the shares of the listed

corporation, then state the date that you became aware that you had such an

interest in the shares in Box 2. |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Box 3 |

State the stock code of the listed corporation in

whose shares you are interested. You can find the stock code on the HKEX

website. Alternatively you can get it from the corporation itself. If you file this Form to disclose your interests in

any class of shares of the listed corporation which is not listed on the SEHK

(e.g. “A” shares or domestic shares), state the stock code of the class of

shares of the listed corporation which is listed on the SEHK. |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Box 4 |

Complete the name of the listed corporation in whose

shares you are interested. The system

will auto-fill the name of the listed corporation based on the date of

relevant event in Box 1 and the stock code in Box 3. |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Box 5 |

Select the class of shares in

which you are interested. Some corporations have more than one class of share

capital, each with voting rights (e.g. “A” and “H” shares). If you have an

interest in 5% or more in each of two classes of shares, complete a separate

Form 1 for each class of shares.

However, if you file this Form to disclose your interests in ordinary

shares and preference shares as share stapled units of a listed corporation,

you need not complete two separate Form 1. If you select “Other”, state the

class of shares in which you are interested in Box 24. |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Box 6 |

State the number of shares (in the class of shares in which you are interested) which

have been issued

at the date of the relevant event. You can find the number of

shares issued on the HKEX website by clicking the link to the HKEX website on

the Form or you can ask the corporation. |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Boxes 7 to 13 |

State your personal details

as indicated. State your name in full as it appears

on your Hong Kong identity card

(“HKID Card”). If you have no HKID

Card, state your name

in full as it appears on your passport. If you are a PRC resident who does

not have a HKID Card or a passport, state your name as it appears on your PRC

Resident Card. For example, a substantial shareholder whose name appears on

his HKID Card as “Wong Ging Teng Anthony” would complete Box 7 as follows :

Whereas a substantial shareholder who has no HKID

Card and whose name appears in his passport as “Anthony James Hay Wood” would

complete Box 7 as follows :

You need not fill in Boxes 10 and 11 if you do not

have a Chinese name. Equally you need not fill in Box 7 if you do not have an

English name. You must provide an email address in Box 13. The data entered in Boxes 8, 12 and 13

(i.e. HKID Card/Passport/PRC Resident Card number, daytime telephone number

and email address) will not be available for viewing by the public when

searching the DI pages of the HKEX website. If you have no HKID Card/passport/PRC Resident Card,

select “Others” in Box 8 and provide details

of your

identification document under “HKID Card/Passport/PRC Resident Card number”

column in Box 8. |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Box 14 |

State details of the relevant event (i.e. the event

that triggers the notice). In the case of relevant events (i) to (vi) in

General Note 5 the details that you must give in Box 14 relate to the shares

bought/sold or involved at that time – not the shares which you already have.

Where the relevant event is prompted by a transaction that forms part of a

series of transactions effected on the same day, the details of the relevant

event that you give in Box 14 shall relate to all shares in which you

acquired an interest, ceased to have an interest or the nature of your

interest changed on that day as a result of that series transactions. “Brief

description of relevant event” column State the description which best describes the relevant

event either by entering the Code from Table

1 or selecting the Code from the menu. If a person connected with you

acquired an interest in shares, their interest may be treated as your

interest (See General Note 8 above). For example, if a company that you

control first acquired 5% or more of the shares of the listed corporation,

such company would use the Code 1001 and you should treat the acquisition as

your acquisition and use the appropriate Code – in this case Code 1001 if you

did not already have a notifiable interest yourself. Use the “short position” row if you are filing the

notice because of a change in a short position. The normal position is that

either a long position or a short position will give rise to a duty of

disclosure (not both simultaneously). In the case of an Initial Notification in Box 14,

you need only to complete the column “Brief description of relevant event”

(as the notification is not prompted by an acquisition or disposal of an

interest in shares). See Table 1

for the Codes of Relevant Events. “Capacity

in which shares were/are held” column State the description which best describes the

capacity in which the shares were/are held before and after the relevant

event either by entering the Code from Table

2 or selecting the Code from the menu. If you have disposed of an

interest in shares, select the Code describing the capacity in which you held

the shares immediately before the disposal and enter this Code in the “Before

relevant event” column. If you have acquired an interest in shares, select

the Code describing the capacity in which you held the shares immediately

after your acquisition and enter this Code in the “After relevant event”

column. If you are giving a notice of a change in the nature of your interest

in shares, select the Codes describing the capacity in which you held your

interest in those shares before and after the relevant event, i.e. complete

both the “Before relevant event” and “After relevant event” columns. If you

are, or were, the beneficial owner but another Code also applies, please use

the latter Code rather than 2101. If

you ceased to have an interest in at least 5% of the shares in the listed

corporation after the relevant event, you must use Code 1704 and describe the

relevant event in Box 24. Use the “short position” row if you are filing

because of a change in a short position. See Table 2

for the Codes of Capacity. “Number of

shares bought/sold or involved” column State the number of shares concerned (e.g. the number

of shares you bought that triggered the notice). For a change in the nature

of an interest (e.g. on exercise of an option), state the number of shares

affected by the change. “Currency

of transaction” column Select the currency in which the price for the

interest in shares described in the “Number of shares bought/sold or

involved” column was paid or received. “On

Exchange” and “Off Exchange” columns State the consideration per share paid or received

for the interests in shares described in the “Number of shares bought/sold or

involved” column in the “On Exchange” or “Off Exchange” columns as

appropriate. An acquisition or disposal is made “On-Exchange” when the

transaction took place in the ordinary course of trading on a recognized

exchange and “Off-Exchange” covers all other transactions. For an on-exchange

transaction, state the highest price per share in the “Highest price (per

share)” column and the average price/consideration per share in the “Average

price (per share)” column. For an off-exchange transaction, state the average

price/consideration per share in the “Average consideration (per share)”

column and select a Code which best describes the nature of the consideration

you paid or received in the “Nature of consideration” column. If no price or consideration has been paid or

received, or if the consideration is services provided, the price or

consideration should be stated as “0”. If the transaction that prompts

disclosure is a change in nature of your interest in shares (e.g. a

securities borrowing and lending transaction), a transaction in derivatives,

or a change in short position, the highest price per share and the average

price per share (average consideration per share and nature of the consideration

for off-exchange transactions) should be left blank. See Table 3

for the Codes of Nature of Consideration. Example of how to complete Box 14 Assume that you already own 4,500,000 shares in the listed corporation

or 4.5% of the shares

in issue. On 31 December 2003, you purchased (through the SEHK)

400,000 shares for HK$800,000 and

100,000 shares for HK$210,000 (all shares to be held beneficially) increasing your total shareholding to 5%.

As the two transactions are a series of transactions on the same

date the details of the relevant event that you give in Box 14 shall relate to the purchase of 500,000 shares which is the relevant

event. The date of the relevant event to be inserted

in Box 1 would be “31.12.2003” and you should

complete Box 14 in the following manner. The Codes to be used are described below. Details of

relevant event

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

* Due to

limited space in these Notes, the description of relevant event and capacity

in which shares were/are held are not shown but will be displayed in the

Form. |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Box 15 |

State the total number of shares in which you were

interested, and those in which you had a short position (if any), immediately

before the relevant event in column 2. This figure includes all joint

interests, interests through equity derivatives and deemed interests (See

General Note 8 above). State the percentage figure of your interest, your

short position (if any), immediately before the relevant event in column 3.

General Note 7 above explains how you calculate the percentage figure. If you file this Form to disclose any interests in

the shares in a lending pool, together with your other interests in the

shares, do not aggregate your interests in the lending pool with your

other interests in which you had a long position or a short position. In the case of an Initial Notification, you need not

complete Box 15. |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Box 16 |

State the total number of shares in which you were

interested, and those in which you had a short position (if any), immediately

after the relevant event in column 2. This figure includes all joint

interests, interests through equity derivatives and deemed interests (See

General Note 8 above). State the percentage figure of your interest, your

short position (if any), immediately after the relevant event in column 3.

General Note 7 above explains how you calculate the percentage figure. |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Box 17 |

State the description which best describes the

capacity in which you hold the shares or short position listed in Box 16

either by entering the Code from Table

2 or selecting the Code from the menu in column 1. If you hold some of

your interests in one capacity (e.g. as beneficial owner), and other

interests in other capacity (e.g. as trustee), then use two Codes (on

different rows) and the number of the interests in shares held in each

capacity (in different rows) in column 2 (or 3). |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Box 18 |

If you derive all or part of your interest in shares

(or your short position) which are listed in Box 16 from equity derivatives,

state the description which best describes the derivatives that you hold

either by entering the Code from Table

4 or selecting the Code from the menu in column 1. State the number of

shares in which you derive an interest (or a short position) from the

derivatives in column 2 (or 3). General Note 13 explains how to work this

out. If you have more than one derivative of the same

category, add them together and state the total number (in one row) in column

2 (or 3). If you have more than one derivative but they are in different

categories, use two or more Codes (on different rows) and state the number of

shares for each category of derivative (on different rows) in column 2 (or

3). If any party to a derivative can choose whether to

settle in cash or by delivery, treat that derivative as physically settled. See Table 4

for the Codes of Category of Derivatives. |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Box 19 |

If your spouse (or child under 18) is interested in

shares in the same listed corporation, add your spouse’s interest/your

child’s interest to your interests in calculating whether you are under a

duty of disclosure. Details of that interest must also be taken into account

in completing Boxes 14 to 18. State the name of the spouse/child, his/her

address and the number of shares in which he/she is interested. State the

details of each additional family member who holds shares in the listed

corporation. If your family member also has a short position,

then the same principles apply. The data entered in column 3 (i.e. address of spouse

and/or children) will not be available for viewing by the public when

searching the DI pages of the HKEX website. |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Box 20 |

If you are entitled to exercise, or control the

exercise of, one-third or more of the voting power at general meetings of a

corporation, or the corporation or its directors are accustomed to act in

accordance with your directions, and that corporation is interested in shares

of the listed corporation concerned, give details of that corporation

(referred to in these Notes as a “controlled corporation”). If there is more

than one corporation that you control, then details of each controlled

corporation must be stated separately in Box 20. You must also add the controlled corporation’s

interest to your interests in working out whether you are under a duty of

disclosure and when completing Boxes 14 to 18. If the corporation that you

control also has a short position, then the same principles apply. Box 20 should be completed as follows :

Example of

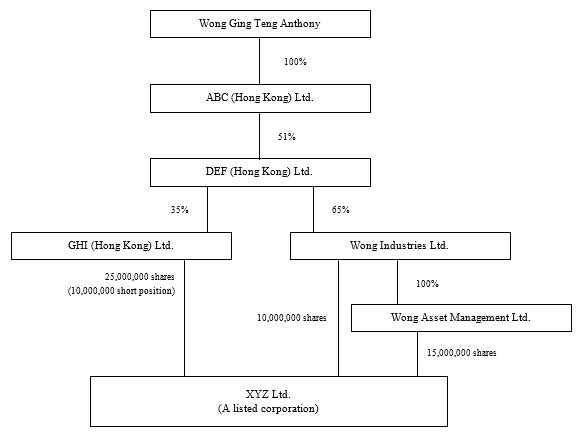

how to complete Box 20 Assume that Mr. Wong Ging Teng Anthony owns 100% of

the shares in a private corporation ABC (Hong Kong) Ltd. which owns 51% of

the shares in DEF (Hong Kong) Ltd. which owns 35% of GHI (Hong Kong) Ltd. and

65% of Wong Industries Ltd. Wong Industries Ltd. in turn owns 100% of the

shares in Wong Asset Management Ltd. The group holdings in XYZ Ltd. (a listed

corporation) are as follows : GHI (Hong Kong) Ltd. has a call option over

25,000,000 shares (physically settled) and has a short position in 10,000,000

shares under a cash settled equity derivative (details of these derivative

interests will have been given in Box 18). Wong Industries Ltd. owns

10,000,000 shares and Wong Asset Management Ltd. owns 15,000,000 shares. Group

structure and holdings :

In this example, the entries in

Box 20 would be as follows : 20. Further

information in relation to interests of corporations controlled

by substantial shareholder

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Box 21 |

If you are interested in shares of the listed

corporation concerned jointly with another person, you are both taken to be

interested in all of the shares held jointly in calculating whether you have

to file a notice, and in completing Boxes 14 to 18. State the name of the

person who owns the interest in the shares jointly with you, his/her/its

address and the number of shares in which he/she/it is interested. The same

principles apply to short positions held jointly. |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Box 22 |

If you are a trustee of a trust, a beneficiary of a

trust, or if you are the “founder” of a discretionary trust (e.g. you had a

discretionary trust set up or you put assets into it) and can influence how

the trustee exercises his discretion, then add all of the shares in which the

trust has an interest (or a short position) to your interests in working out

whether you must file a notice. Disclose details of that interest (or short

position) when completing Boxes 14 to 18. You need not state the name of the trust

which owns the interest in the shares and its address in columns 1 and 2 if

you wish these to remain private.

State the description which best describes your status in relation to

the trust either by entering the Code from Table 5 or selecting the Code from the menu in column 3. State

the number of shares in which the trust is interested (or has a short

position) in column 4 (or 5). Ignore an interest in reversion or remainder,

an interest of a bare trustee, and any discretionary interest (of a beneficiary). See Table 5

for Codes of Status in relation to a Trust. |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Box 23 |

If you are a party to an agreement with other

parties to acquire interests in shares in the listed corporation concerned in

the circumstances set out in section 317(1)(a) or (b) of the SFO, then add

any shares in which any other party to the agreement is interested to your

own interests in working out whether you must file a notice. Details of the

interests of any other party must also be taken into account in completing

Boxes 14 to 18. You must state the name of each of the other parties to the

agreement, his/her/its address and the number of shares in which he/she/it is

interested “apart from the agreement” in Box 23. In the last row of Box 23,

state the number of shares in which you are interested under sections 317 and

318 of the SFO. This will be the total of firstly all shares which have been

purchased pursuant to the agreement by any of the parties to the agreement

and secondly all shares in which the other parties to the agreement are

interested “apart from the agreement” (defined in section 318(2) of the SFO).

Example of

how to complete Box 23 Assume that

Mr. Wong Ging Teng

Anthony and 2 other persons agree to buy shares

in XYZ Ltd. (a listed corporation). They

are each already

interested in a number of shares

of XYZ Ltd. which

they purchased before they entered into the s.317 agreement.

Under the s.317 agreement, Mr.

Wong purchased 25,000,000 shares, Mr. A purchased 20,000,000 shares and Mr. B

purchased 15,000,000 shares in XYZ Ltd. Their shareholdings are as follows –

Assume also that Mr. Wong is completing the notice.

He will already have stated in Box 16 that he is interested in 116,000,000 shares.

He has to state the number of shares in which the other parties are

interested “apart from the agreement” and the total shares in which he is

interested by the application of sections 317 and 318 (the 60,000,000 shares

bought pursuant to the agreement and the further shares that the other

parties are interested in “apart from the agreement”). Accordingly, Mr. Wong

will then complete Box 23 as follows – 23. Further information

from a party to an agreement under

section 317 (Please see

Notes for further information

required)

You must

also - (i)

attach a separate sheet to the notification stating

that you are a party to an agreement to which section 317(1)(a) or (b)

applies; (ii)

include a copy of any written agreement, contract or

other document which records any terms or details of the agreement; and (iii)

if there are no such papers as are mentioned in

(ii), or if such papers do not record the material terms of the agreement,

include a written memorandum setting out the material terms of the agreement. If the agreement or document required under (ii)

records terms or details other than any arrangement to which section

317(1)(a) or (b) applies, you need to provide the extracts of the agreement

or document which relates to any arrangement to which section 317(1)(a) or

(b) applies. The memorandum required under (iii) should include

details of any cash or consideration involved and the identity of all persons

between whom such cash or other consideration is passed or is intended to

pass. If the parties are interested in any derivatives, the exercise or

conversion price, expiration date and exercise period should be disclosed.

The memorandum must be signed by the substantial shareholder or his duly

authorized agent. A notification that a person has ceased to be a

party to an agreement to which section 317(1)(a) or (b) applies shall also

state that he or the other party (as the case may be) has ceased to be a

party to the agreement and, in the latter case, include the name and address

of the other party. Copies of any documents that are submitted to the

SEHK by using the DION System will be available for inspection by the public

on HKEX website. If you wish to keep any personal information in private,

redact such information before submitting the document. Do not

submit copies of any documents which are password-protected or otherwise

encrypted so as to ensure the documents can be properly opened and displayed

on the DI pages of the HKEX website. |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Box 24 |

Provide any supplementary information, e.g. the

class of shares if you select “Other” in Box 5; the description of the

relevant event if you select Code 1013 (any other event), Code 1113 (any

other event), Code 1213 (any other event), Code 1316 (any other event), Code

1403 (any other event), Code 1503 (any other event), Code 1702 (Notice filed

to remove outdated information), Code 1704 (Notice filed because you ceased

to have a notifiable interest in the shares of the listed corporation), Code

1710 (Voluntary disclosure) or Code 1711 (Other); the capacity if you select

Code 2501; the category of derivatives if you select Code 4104 or 4108. The word limit of this Box is 500 characters of text

and numbers. |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Box 25 |

Tick this box if this Form 1 is a

revision of a previously submitted Form and insert the log/serial number of

the Form which you intend to revise. |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Box 26 |

State the

number of document stating that you are a party to an agreement to which

section 317(1)(a) or (b) applies, concert party agreement or memorandum in

relation to any agreement to which you are a party to acquire interests in

shares listed in Box 23. Do not

send copies of share purchase agreements and other documents to the SEHK when

filing this Form. Attaching a document that explains the transaction in

question does not discharge

the duty to complete the prescribed form. |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Special Notes

Substantial shareholders who are also directors

or chief executives

should use Form 3A

1.

If you are a person who is both a substantial

shareholder and a director of the listed corporation concerned,

you may have separate duties

to file notices (one in each capacity) as a result of a single event. For example,

a person who is interested

in 5.9% of the shares of a listed corporation and buys a further 0.2% will have to file a notice because he is a director

(and therefore has to disclose all transactions) and will also have to file a notice as a substantial shareholder because

his interest has crossed the 6% level.

2.

If you are substantial shareholder and also a director then you must use Form 3A (Director/Chief

executive

Notice) to discharge your duty to disclose your interests (short position) in your capacity as both a substantial shareholder and as a director. This avoids the need to file both Form 1 and Form 3A.

Securities Borrowing and Lending

If you control an ALA and are

giving notification under section 5(4) of the Securities and Futures

(Disclosure of Interests – Securities Borrowing and Lending) Rules (Cap.571X)

(“SBL Rules”) then you need only complete Boxes 1 to 13, columns the “Brief

description of relevant event” and the “Number of shares bought/sold or

involved” columns of Box 14, Boxes 15 to 17, 19 to 21 of Form 1. All boxes

should be completed in accordance with the Specific Notes set out above with

the exception of Boxes 15 and 16. Boxes 15 and 16 should be completed as

follows.

Box 15 In

column 2 of Box 15, state the total number of shares in which you were

interested, and those in which you had a short position, immediately before

the relevant event. In column 3, state the percentage figure of your interest,

and short position (if any), immediately before the relevant event. You should

include shares that the ALA is authorized to lend in the total of shares in

which you are interested when completing row 1 of columns 2 and 3 of Box 15.

In column 2, row 3 of Box 15 (labelled “Lending

pool”), state only the number of shares that the ALA is authorized to lend

immediately before the relevant event (referred to as “qualified shares” in the

SBL Rules). In column 3, row 3 of Box 15, state the percentage figure of the

interest of the ALA in qualified shares immediately before the relevant event.

Box 16 Complete

rows 1 and 2 of Box 16 in the same manner as Box 15 specifying the total number

of shares in which you were interested, and those in which you had a short

position immediately after the relevant event.

In

column 2, row 3 of Box 16 (labelled “Lending pool”), state only the number of

shares that the ALA is authorized to lend (i.e. “qualified shares”) immediately

after the relevant event. In column 3, row 3 of Box 16, state the percentage

figure of the interest of the ALA in qualified shares immediately after the

relevant event.

Table 1 –

Codes of Relevant Events

Please note that :

(1)

It may be necessary to go through two to three levels

of questions before reaching the relevant event and an event code is only

assigned to the last level of question. Code numbers in brackets are interim

level(s) of questions and they are not event codes. Only the ultimate event

codes will be available for selection.

(2)

The same set of event codes apply to all Forms so some

code numbers are “skipped” because certain events are not relevant to this

Form.

(3)

The term “your

interest/short position” in these event codes refers to your own interest/short

position and also includes an interest/short position of your spouse, your

minor child or a corporation that is controlled by you, that is taken to be

your interest/short position by attribution.

(4)

The “shares” are the voting

shares in the listed corporation.

|

Code No. (Level 1) |

Code No. (Level 2) |

Code No. (Level 3) |

Description of event (Box 14) |

|

(100) |

|

|

You first acquire a notifiable interest because: |

|

(110) |

|

|

The percentage level of your interest in the shares

has increased because: |

|

(120) |

|

|

The percentage level of your interest in the shares

has reduced because: |

|

(130) |

|

|

There has been a change in nature of your interest

in the shares because: |

|

(140) |

|

|

You came to have a short position of 1% or more in

the shares, or the percentage level of your short position in such shares

increased because: |

|

(150) |

|

|

You ceased to have a short position of 1% or more in

the shares, or the percentage level of your short position in such shares

decreased because: |

|

(160) |

|

|

Approved Lending Agents |

|

(170) |

|

|

Miscellaneous |

|

|

|

|

|

|

(100) |

|

|

You first

acquire a notifiable interest because: |

|

|

1001 |

|

you purchased

the shares |

|

|

1002 |

|

you were given

the shares |

|

|

(1003) |

|

you became the

holder of, wrote or issued equity derivatives under which (choose one): |

|

|

|

10031 |

you have a right

to take the underlying shares |

|

|

|

10032 |

you are under an

obligation to take the underlying shares |

|

|

|

10033 |

you have a right

to receive from another person an amount if the price of the underlying

shares is above a certain level |

|

|

|

10034 |

you are under an

obligation to pay another person an amount if the price of the underlying

shares is below a certain level |

|

|

|

10035 |

you have any of

the rights or obligations referred to in 10031 to 10034 above embedded in a

contract or instrument |

|

|

1004 |

|

you acquired a

security interest in the shares |

|

|

1005 |

|

you inherited

the shares |

|

|

1006 |

|

you became a

beneficiary under a trust interested in the shares |

|

|

1007 |

|

you took steps

to enforce your rights in the shares you hold by way of security as a

qualified lender |

|

|

1009 |

|

you entered into

an agreement for the exchange of an instrument for another instrument in

respect of the same underlying shares |

|

|

1010 |

|

you were placed

the shares as a placee under a top-up placing |

|

|

1011 |

|

new shares were

issued to you after you have reduced your interest in shares by placing them

to placee(s) under a top-up placing |

|

|

1012 |

|

you became a

member of a concert party group or a member of the concert party group

acquired more of the shares |

|

|

1013 |

|

any other event (you

must briefly describe the relevant event in the Supplementary Information

box) |

|

(110) |

|

|

The percentage

level of your interest in the shares has increased because: |

|

|

1101 |

|

|

|

|

1102 |

|

you were given

the shares |

|

|

(1103) |

|

you became the

holder of, wrote or issued equity derivatives under which (choose one): |

|

|

|

11031 |

you have a right

to take the underlying shares |

|

|

|

11032 |

you are under an

obligation to take the underlying shares |

|

|

|

11033 |

you have a right

to receive from another person an amount if the price of the underlying

shares is above a certain level |

|

|

|

11034 |

you are under an

obligation to pay another person an amount if the price of the underlying

shares is below a certain level |

|

|

|

11035 |

you have any of the

rights or obligations referred to in 11031 to 11034 above embedded in a

contract or instrument |

|

|

1104 |

|

you acquired a

security interest in the shares |

|

|

1105 |

|

you inherited

the shares |

|

|

1106 |

|

you became a

beneficiary under a trust interested in the shares |

|

|

1107 |

|

you took steps

to enforce your rights in the shares you hold by way of security as a

qualified lender |

|

|

1109 |

|

you entered into

an agreement for the exchange of an instrument for another instrument in

respect of the same underlying shares |

|

|

1110 |

|

you were placed

the shares as a placee under a top-up placing |

|

|

1111 |

|

new shares were

issued to you after you have reduced your interest in shares by placing them

to placee(s) under a top-up placing |

|

|

1112 |

|

you became a member

of a concert party group or a member of the concert party group acquired more

of the shares |

|

|

1113 |

|

any other event

(you must briefly describe the relevant event in the Supplementary

Information box) |

|

(120) |

|

|

The percentage

level of your interest in the shares has reduced because: |

|

|

1201 |

|

|

|

|

1202 |

|

you made a gift

of the shares |

|

|

1203 |

|

you delivered

the shares or an amount due under equity derivatives |

|

|

(1204) |

|

expiry or cancellation

without exercise of equity derivatives under which (choose one): |

|

|

|

12041 |

you had a right

to take the underlying shares |

|

|

|

12042 |

you were under

an obligation to take the underlying shares |

|

|

|

12043 |

you had a right

to receive from another person an amount if the price of the underlying

shares was above a certain level |

|

|

|

12044 |

you were under

an obligation to pay another person an amount if the price of the underlying

shares was below a certain level |

|

|

|

12045 |

you had any of the

rights or obligations referred to in 12041 to 12044 above embedded in a

contract or instrument |

|

|

1205 |

|

you ceased to

have a security interest in the shares |

|

|

1206 |

|

you did not take

up, or sold, rights in a rights issue |

|

|

1208 |

|

you entered into

an agreement for the exchange of an instrument for another instrument in

respect of the same underlying shares |

|

|

1209 |

|

you placed the

shares to placee(s) under a top-up placing |

|

|

1210 |

|

new shares were

issued in a top-up placing |

|

|

1211 |

|

you have ceased

to be a member of a concert party group or a member of the concert party

group has disposed of some of the shares |

|

|

1213 |

|

any other event

(you must briefly describe the relevant event in the Supplementary

Information box) |

|

(130) |

|

|

There has been a

change in nature of your interest in the shares because: |

|

|

1301 |

|

the shares have been delivered to you and you have not previously notified the purchase of the shares |

|

|

1302 |

|

you have entered

into an agreement for the sale of shares in which you are interested but are

not required to deliver them within 4 trading days |

|

|

1303 |

|

you have

exercised rights to the shares under equity derivatives |

|

|

1304 |

|

rights to the

shares under equity derivatives have been exercised against you |

|

|

1305 |

|

you have provided

an interest in the shares as security to a person other than a qualified

lender |

|

|

1306 |

|

an interest in

the shares, that you provided as security to a person other than a qualified

lender, has been released |

|

|

1307 |

|

you have taken

steps to enforce a security interest in the shares, or rights to such shares

held as security, and you are not a qualified lender |

|

|

1308 |

|

steps have been

taken to enforce a security interest in the shares, or rights to such shares

held as security, against you |

|

|

1309 |

|

you are a

beneficiary under a will and the shares have been transferred to you by an

executor |

|

|

1310 |

|

you are a

beneficiary under a trust and the shares have been transferred to you by a

trustee |

|

|

1311 |

|

you have

delivered the shares to a person who had agreed to borrow them |

|

|

1312 |

|

the shares lent

by you have been returned to you |

|

|

1313 |

|

you have lent

the shares under a securities borrowing and lending agreement |

|

|

1314 |

|

you have

recalled the shares under a securities borrowing and lending agreement |

|

|

1315 |

|

you have

declared a trust over shares that you continue to hold |

|

|

1316 |

|

any other event

(you must briefly describe the relevant event in the Supplementary

Information box) |

|

(140) |

|

|

You came to have

a short position of 1% or more in the shares, or the percentage level of your

short position in such shares increased because: |

|

|

(1401) |

|

you became the holder of, wrote or issued equity derivatives under

which (choose one): |

|

|

|

14011 |

you have a right

to require another person to take delivery of the underlying shares |

|

|

|

14012 |

you are under an

obligation to deliver the underlying shares |

|

|

|

14013 |

you have a right

to receive from another person an amount if the price of the underlying

shares is below a certain level |

|

|

|

14014 |

you are under an

obligation to pay another person an amount if the price of the underlying

shares is above a certain level |

|

|

|

14015 |

you have any of

the rights or obligations referred to in 14011 to 14014 above embedded in a

contract or instrument |

|

|

1402 |

|

you borrowed the

shares under a securities borrowing and lending agreement |

|

|

1403 |

|

any other event

(you must briefly describe the relevant event in the Supplementary

Information box) |

|

(150) |

|

|

You ceased to

have a short position of 1% or more in the shares, or the percentage level of

your short position in such shares decreased because: |

|

|

(1501) |

|

expiry or

cancellation without exercise of equity derivatives under which (choose one): |

|

|

|

15011 |

you have a right

to require another person to take delivery of the underlying shares |

|

|

|

15012 |

you are under an

obligation to deliver the underlying shares |

|

|

|

15013 |

you have a right

to receive from another person an amount if the price of the underlying

shares is below a certain level |

|

|

|

15014 |

you are under an

obligation to pay another person an amount if the price of the underlying

shares is above a certain level |

|

|

|

15015 |

you have any of

the rights or obligations referred to in 15011 to 15014 above embedded in a contract

or instrument |

|

|

1502 |

|

you returned the

shares borrowed under a securities borrowing and lending agreement |

|

|

1503 |

|

any other event

(you must briefly describe the relevant event in the Supplementary

Information box) |

|

(160) |

|

|

Approved Lending

Agents |

|

|

(1601) |

|

|

|

|

|

16011 |

the percentage level

of your interest in the shares held in your lending pool is taken to have

increased |

|

|

|

16012 |

the percentage

level of your interest in the shares held in your lending pool is taken to

have reduced |

|

|

(1602) |

|

Notice under

section 5(4) of the Securities and Futures (Disclosure of Interests –

Securities Borrowing and Lending) Rules by a person that controls an approved

lending agent (choose one): |

|

|

|

16021 |

the percentage

level of your interest in the shares held in the lending pool of the approved

lending agent is taken to have increased |

|

|

|

16022 |

the percentage

level of your interest in the shares held in the lending pool of the approved

lending agent is taken to have reduced |

|

(170) |

|

|

Miscellaneous |

|

|

1701 |

|

On listing of the corporation or a class of shares of the listed

corporation |

|

|

1702 |

|

Notice filed to

remove outdated information (if you select this Code you must state the

outdated information in the Supplementary Information box and identify the

box which contains the updated information) |

|

|

1703 |

|

Notice filed

because of a change in the threshold for disclosure |

|

|

1704 |

|

Notice filed

because you ceased to have a notifiable interest in the shares of the listed corporation

(you must briefly describe the relevant event in the Supplementary

Information box) |

|

|

1710 |

|

Voluntary

disclosure (you must briefly describe the relevant event in the Supplementary

Information box) |

|

|

1711 |

|

Other (you must

briefly describe the relevant event in the Supplementary Information box) |

Table 2 – Codes of Capacity

Please note the same set of capacity codes apply to

all Forms so some code numbers are “skipped” because certain capacities are not

relevant to this Form.

|

Code No. |

Description of

the capacity in which you held the interest or short position in shares that

is acquired, disposed of or changed (Boxes 14 and 17) |

|

|

Common capacities |

|

2101 |

Beneficial owner |

|

2103 |

Interests held jointly with another person |

|

2104 |

Agent |

|

2105 |

Underwriter |

|

2106 |

Person having a security interest in shares |

|

|

Interests by attribution |

|

2201 |

Interest of corporation controlled by you |

|

2202 |

Interest of your spouse |

|

2203 |

Interest of your child under 18 years of age |

|

|

Trusts and similar interests |

|

2301 |

Trustee |

|

2304 |

Executor or administrator |

|

2305 |

Beneficiary of a trust (other than a discretionary interest) |

|

2306 |

Nominee for another person (other than a bare trustee) |

|

2307 |

Founder of a discretionary trust who can influence how the trustee

exercises his discretion |

|

|

Persons acting in concert |

|

2401 |

A concert party to an agreement to buy shares described in s.317(1)(a)

|

|

2402 |

A person making a loan or providing security to buy shares described

in s.317(1)(b) |

|

|

Miscellaneous |

|

2501 |

Other (you must describe the capacity in the Supplementary Information

box) |

|

2502 |

Approved lending agent |